Towards a standardised CBDC?

Reading time: 4 minutes. Published on .The European Central Bank is developing the digital euro based on a catalogue of requirements. These, in turn, come from the European Commission’s draft law, among other sources. But if you look beyond Europe, you can see clear differences to the CBDCs of other countries. Is there any prospect of harmonisation at a technical level?

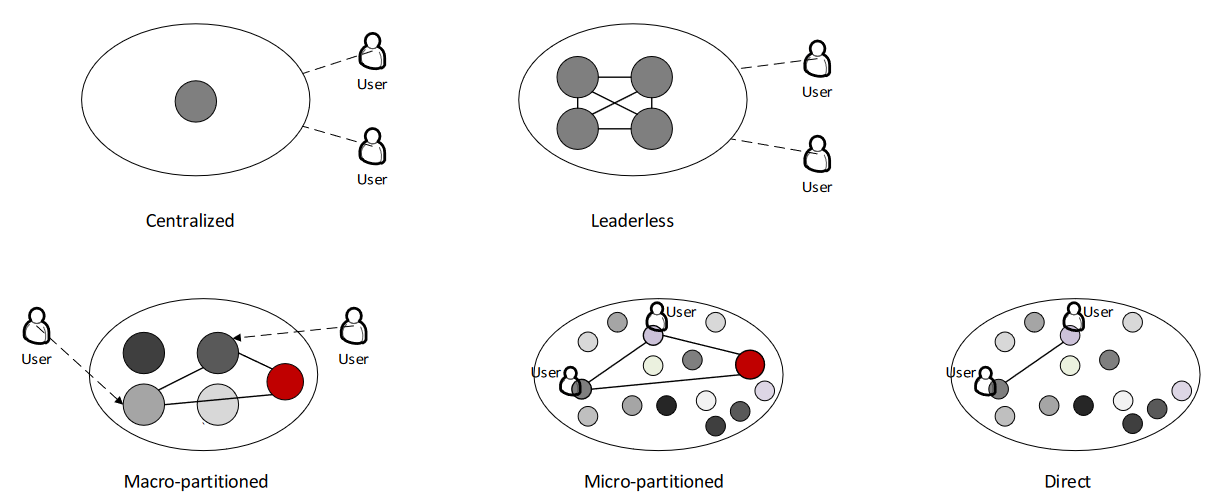

Design options for a CBDC are diverse. Recently, the Bank of Canada discussed a series of so-called ‘archetypes’—i.e. common system design patterns—in a discussion paper. They relate to how transactions are processed, and range from one extreme, namely directly between two devices, to fully centralised via the central bank.

Bank of Canada also identified other dimensions, such as the design of the wallets and the specific representation of monetary values. Not all combinations are suitable for all use cases: For example, offline payment is only possible in the direct model. This is why this model was used in the CBDC pilot projects in Ghana and Thailand.

Some central banks, on the other hand, prefer a centralised approach. These include the Bank of England and the European Central Bank. The digital euro will therefore also come in two versions (online and offline).

As it stands now, there are many CBDC designs, tailored to specific (and perhaps different) use cases and national characteristics. Is this a ‘proliferation’ of incompatible solutions or is standardisation foreseeable? The answer to this question is nuanced. Even today, managing the various payment methods for transactions is already challenging.

We should note that the digital euro is a pan-European payment instrument that is prepared to support multiple currencies. This is also in line with ECB’s strategy, incorporating additional currencies into its systems (e.g. Danish krone) in the past.

This means that the digital euro is already one step ahead of the European schemes that can currently only be used nationally. Standardised interfaces will then ensure that a German wallet can be used in Spain without any problems. And of course, also in online shops.

At the international level, however, integration becomes more difficult. Several committees are currently working on the standardisation of CBDC solutions, including

-

the International Organisation for Standardisation (ISO), specifically Technical Committee 68 on Financial Services;

-

the International Telecommunication Union (ITU);

Not only are new standards required, but existing ones also need to be adapted. For example, the ubiquitous EMV standards for card payments at the checkout only support offline payments to a very limited extent. Other aspects of EMV such as PIN validation, on the other hand, can also be used for CBDC. The Bank of England analysed this in a proof of concept last year. (See also my article on the subject.)

The European Central Bank is also in favour of adapting existing standards as far as possible. Some of these have already been identified in the status report from April of this year.

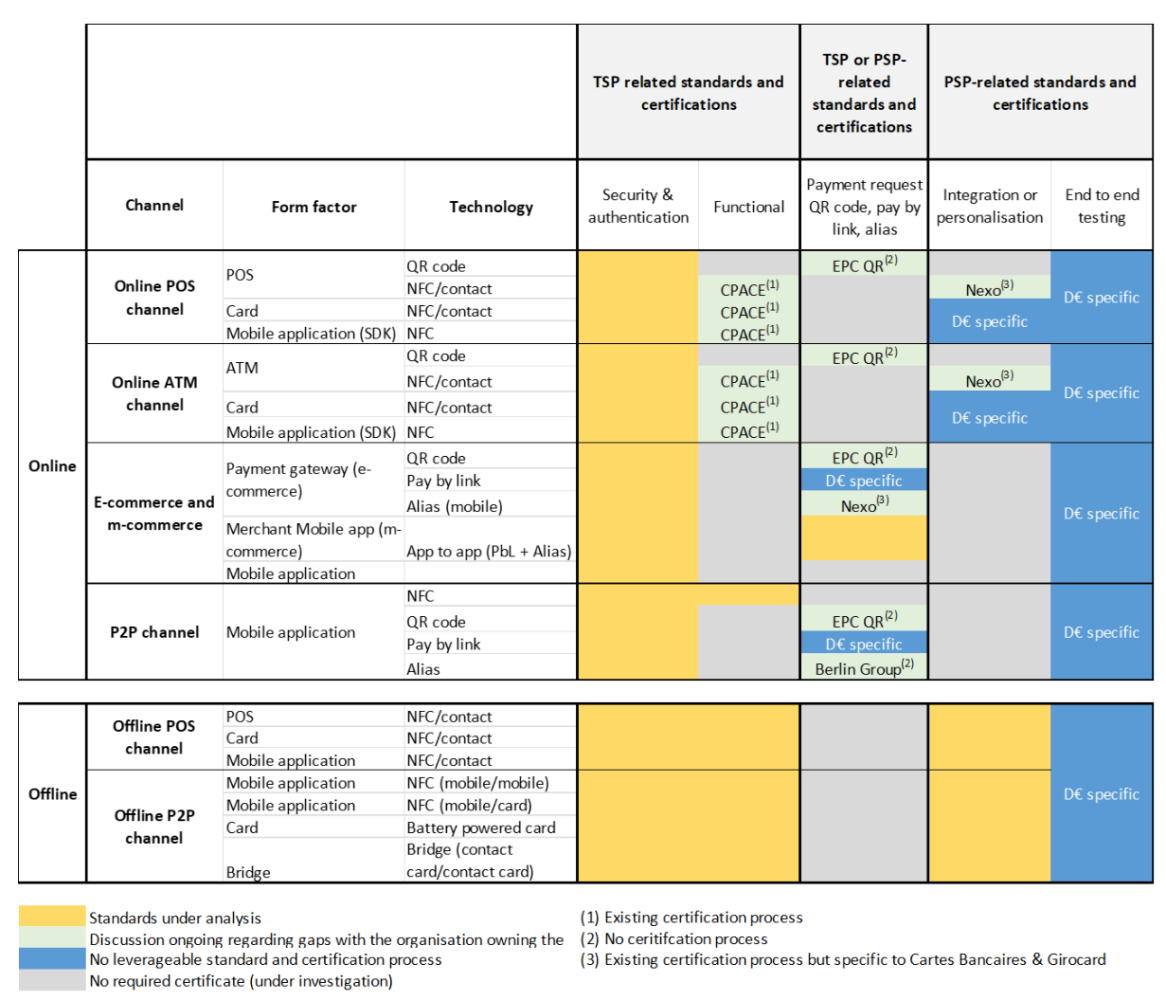

As can be seen from the diagram, some new developments will be necessary for the European market. The situation is similar in other countries that want to introduce a CBDC.

At the international level, standardisation is therefore initially limited to the basics. The aforementioned ISO Committee 68 is currently developing a security model for hardware-based wallets, which only defines security objectives, but not how these are to be implemented. For example, it quickly became clear that different regions would adopt different crypto algorithms: some countries would not accept NIST recommendations and would instead rely on their own. This does not make international compatibility impossible, but it does make it more difficult.

Regardless of this, there is a consensus that international standards such as ISO 20022 will also play a role in the CBDC ecosystem. However, the actual implementation is still unclear, as tokenised payment methods—of which CBDC is one—break with some conventions of the traditional financial world.

Interoperability does not necessarily mean that all CBDCs must have an identical architecture. It can also be achieved through interfaces and agreements between the various banks and central banks, like what is currently the case with international credit cards.

Conclusion

CBDC as a new payment instrument is still at the very beginning of technical harmonisation. Initially, the countries want to adapt it to their own needs; agility is particularly important here. Standardisation, on the other hand, is a lengthy process—already underway—that is based on consensus and requires practical experience.

This post has also been published on LinkedIn.