Cross-border payment: there is no such thing

Reading time: 6 minutes. Published on . Header image credits: Abhijit Chirde on Unsplash.The IMF has recently published a fintech note on cross-border payments with retail CBDC. There is only one problem with it: there is no such thing as a “cross-border payment”.

I am being facetious. Clearly, it is possible to move funds from one country to another country. Under many—if not most—circumstances, I can instruct my bank to transfer money to a foreign account, using the recipient’s IBAN (see an earlier article for an explanation). This process may take a few days, but eventually, the foreign account will be credited with foreign currency.

Then why do I say that there is no such thing?

Because under the hood, a “cross-border payment” is actually multiple payments, each of which using only a single currency. This nuance got lost in the debate.

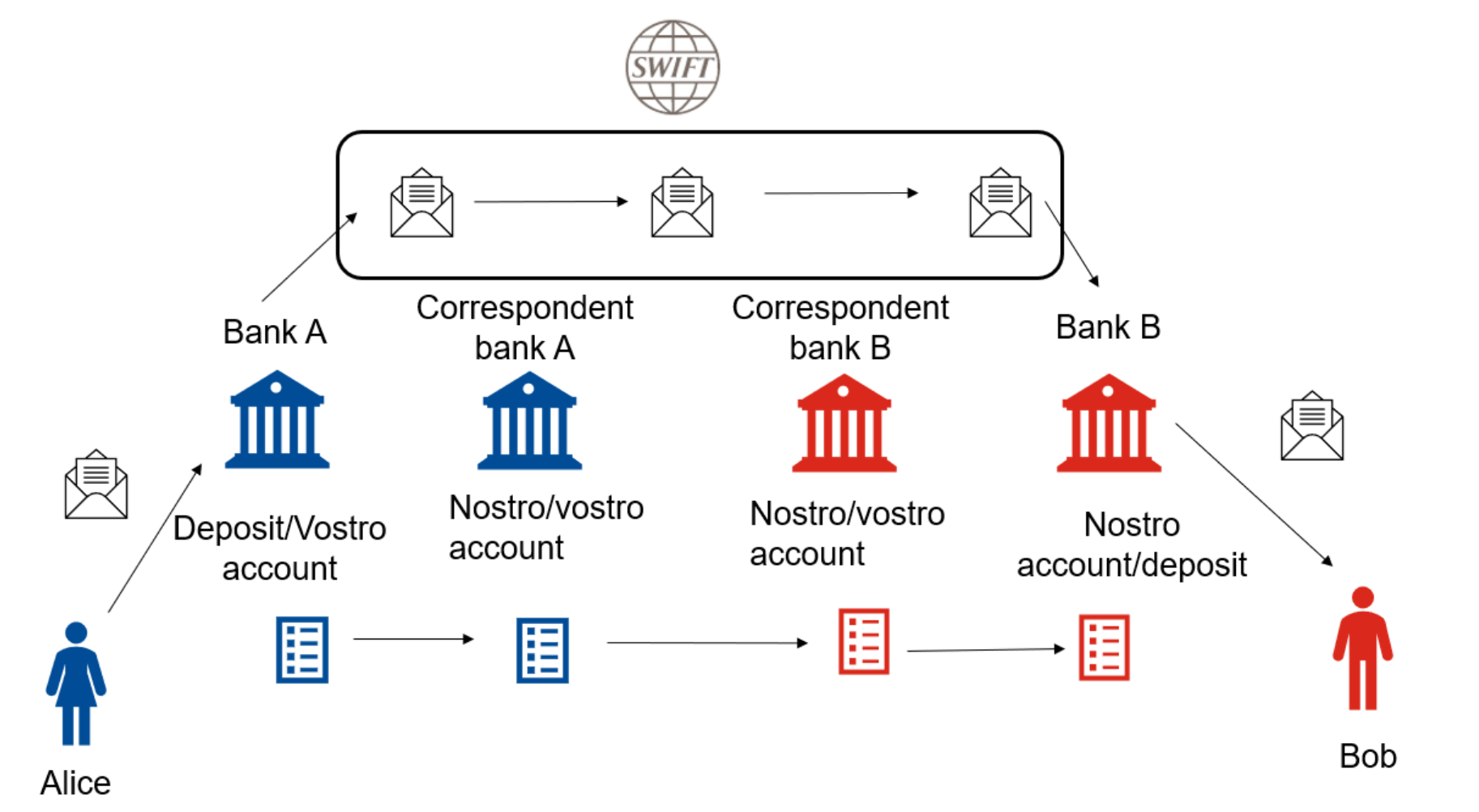

Let us consider a simple example. Assume that Alice owes Bob 10 USD and that she is planning to pay with EUR.

An earlier IMF paper shows a simplified model of how such an international payment would work using the correspondent banking system. The following steps are necessary:

-

Bank A computes the necessary EUR amount based on a market rate (for simplicity, 9 EUR), and debits Alice’s deposit account.

-

The same 9 EUR are credited to Correspondent Bank A, in form of a deposit at Bank A.

-

The actual currency exchange happens between Correspondent Bank A and Correspondent Bank B: The latter receives 10 USD in deposits at Correspondent Bank A.

-

Correspondent Bank B now credits the same 10 USD to Bank B.

-

Bank B can finally credit 10 USD to Bob, which discharges Alice’s obligations.

The paper also presents all six involved balance sheets with a total of twelve bookings. The situation gets worse when more layers of correspondent banks are involved. This can happen for transactions involving less liquid currencies, which are often traded through USD.

As should be obvious, today’s correspondent banking system is fraught with inefficiencies and friction. Since the constituent payments are not settled immediately, every step causes delays and costs. Alice and Bob have limited insight into where their funds are at any given time. Banking systems have different operating hours around the globe. It is not clear which payments should be grouped together to form a chain.

This results in high fees. According to a report, in 2021, sending $200 from Tanzania to Uganda cost an eye-watering $60.

For this reason, some institutions are working on improving cross-border payments. For example, mBridge is a multilateral wholesale CBDC which has started out with four different currencies.

This now brings me to the IMF’s recent fintech note that I mentioned in the beginning. The authors identify five “core elements of a cross-border payment.”

-

Access: the ability of participants to hold and transact currency

-

Communication: the channels and message formats used to transact

-

Currency Conversion: the means and providers of foreign exchange

-

Compliance: the adherence to regulatory requirements in the involved countries

-

Settlement: the actual transfer of funds

As the paper describes, retail CBDC will help in some, but not all these aspects. Clearly, settlement is simplified, because CBDC is a risk-free central bank liability. This means that the number of intermediaries can be reduced.

But like in the traditional correspondent banking system, access remains a challenge. Alice’s bank may not be able to hold USD, perhaps because it has no access to the Federal Reserve’s infrastructure. Conversely, Bob’s bank may not be able to hold EUR.

Closely connected to this is the ability of financial firms to provide currency conversion. Multi-national banks could leverage their access to different countries’ financial infrastructure. In this scenario, if either Alice’s or Bob’s bank can hold both EUR and USD, preferably as retail CBDC, the payment flow becomes much simpler.

Smaller players, however, must rely on a correspondent bank to gain access to a foreign currency. The fintech note correctly states that “this model would defeat some of the benefits of CBDC,” because such indirect holdings “would not be a direct liability of the central bank.” In other words, the credit risk of the traditional system would still be present.

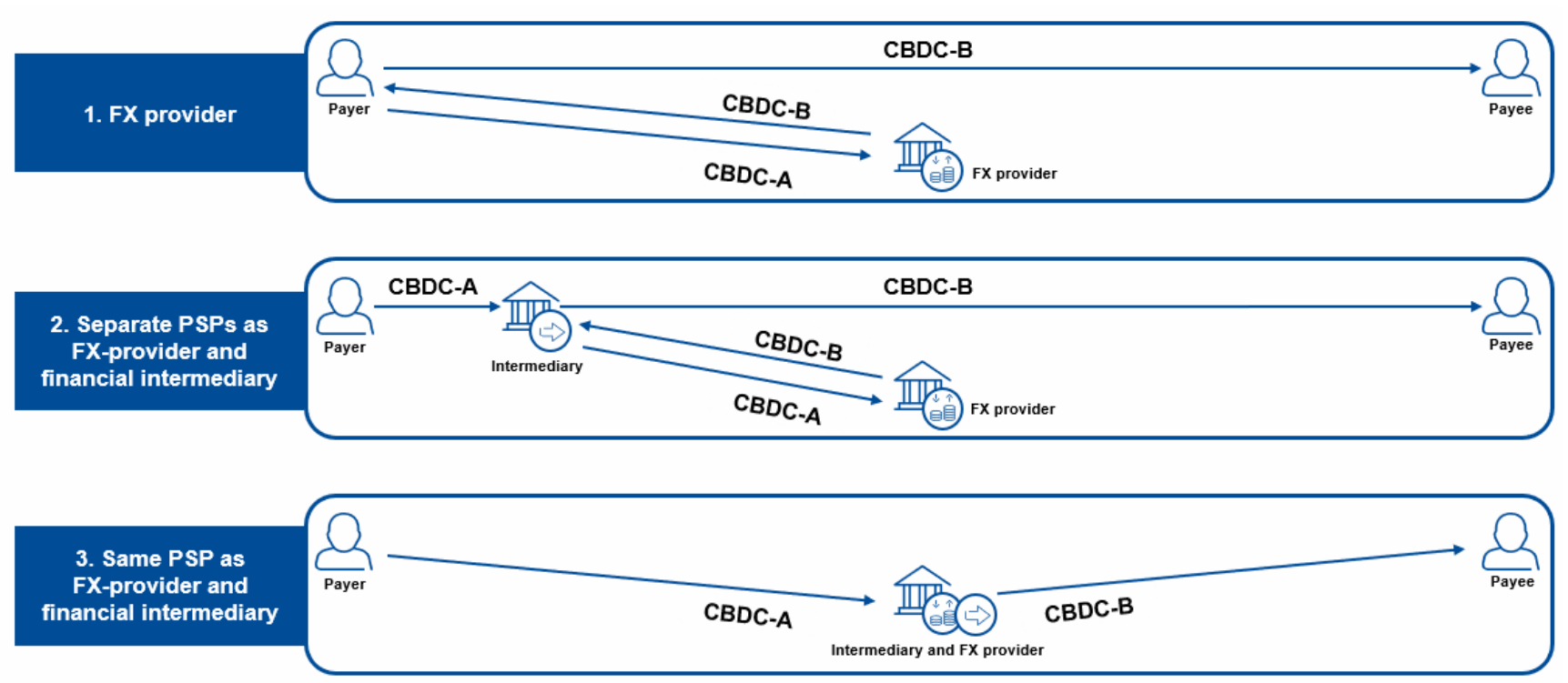

To solve this problem, there is a need for an intermediary that has access to multiple domestic currencies. The IMF sketches three different setups:

The third setup is attractive because it involves the smallest number of constituent payments. However, it would also require central banks and regulators to admit more non-bank intermediaries to take part in their domestic ecosystems. The second setup resembles mBridge and could lead to better competition.

Expanding access also helps to alleviate liquidity for smaller currencies. My colleagues have put forward a set of recommendations to further reduce the cost of currency conversion, including central banks stepping in with swap lines, or multi-lateral trading through automated market makers.

Conclusion

To understand how CBDC can improve payments across borders, we must first understand where the friction in the current system comes from: multiple loosely related payments that are settled individually and with considerable delay.

While CBDC cannot simplify the regulatory framework by itself, it can contribute technical improvements. CBDC is uniquely positioned to foster a more diverse set of intermediaries, because it is an instantly settled asset that carries no counterparty risk. Fintechs interested in providing foreign exchange services would not necessarily manage customer deposits and could therefore be subject to lighter regulation.

In the future, we will probably still not have true cross-border payments. But faster, cheaper, more reliable ones.

Thanks to my colleague Roman Hartinger for fact checking.

References

- Adrian et al.: “A Multi-Currency Exchange and Contracting Platform”, IMF Working Paper 22/217, 2022

- Hartinger and Nagy: “Financial inclusion across borders with retail Central Bank Digital Currencies”, Whitepaper, 2022

- Hupel: “Interoperability aspects of central bank digital currency across ecosystems and borders”, Journal of Payments Strategy & Systems, 17 (4), 422-432

- Reslow, Soderberg, Tsuda: “Cross-Border Payments with Retail Central Bank Digital Currencies: Design and Policy Considerations”, IMF Fintech Notes 2/2024

This post has also been published on LinkedIn.